KEY POINTS

-

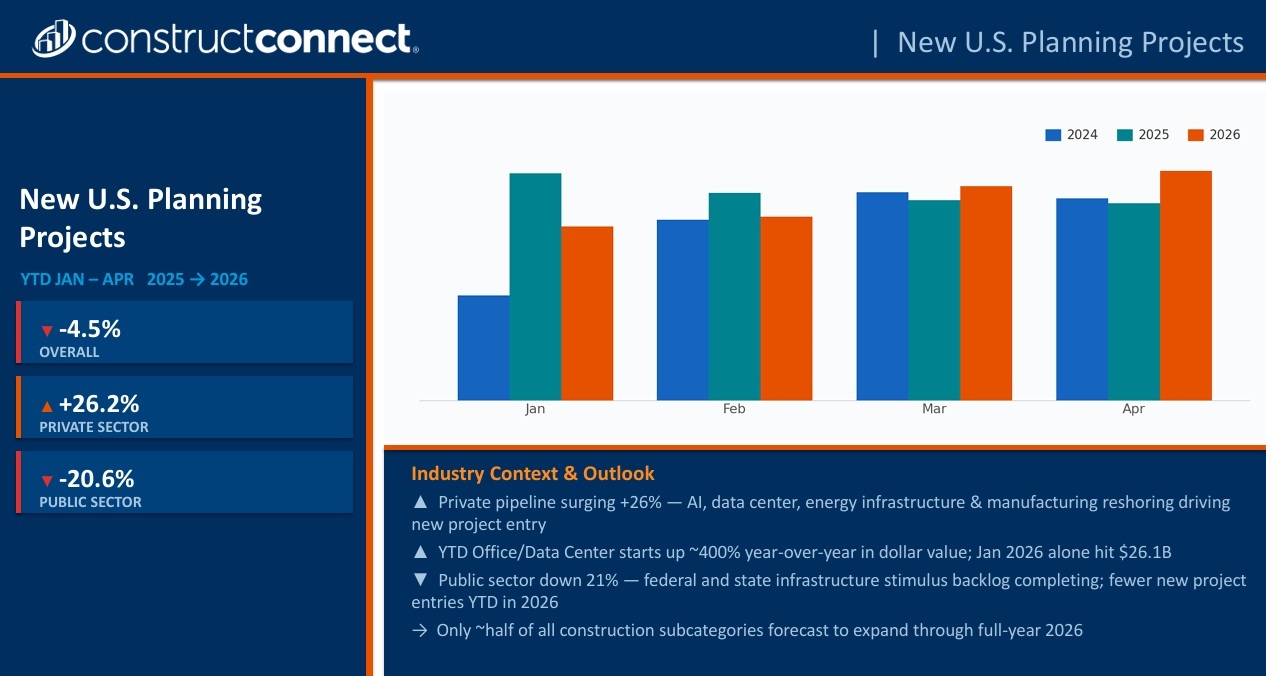

ConstructConnect’s verified planning data shows a split 2026 pipeline: total new U.S. planning fell 4.5%, but private-sector activity rose 26.2% while public-sector planning dropped 20.6%.

-

Private projects are driving opportunity, led by AI, data centers, power infrastructure, and reshoring-related manufacturing investments that tend to appear in planning well before construction begins.

-

Public work remains active, but fewer new public projects are entering the pipeline, making 2026 a selective-growth year where firms need to target the right sectors, geographies, and capabilities.

As Director of Content Acquisition, Kristy O’Brien leads the ConstructConnect team that gathers, verifies, and publishes nonresidential construction project data directly from the owners, architects and contractors behind the work. That vantage point gives her a clear view on what new planning activity is signaling for construction projects in 2026.

The Content Acquisition team at ConstructConnect sits at every stage of the projects we publish. We gather the data, we confirm scope, status and timelines directly with the architects, owners and general contractors doing the work, and then we publish it for customers across the construction industry.

So, when I look at our new U.S. planning numbers, I’m not reading a forecast. I’m describing what is actually coming in the door.

And right now, the new planning is telling two stories on the same chart.

Through the first four months of the year, new U.S. planning entries were down 4.5% compared with the same period in 2025. On its own, that headline reads soft.

But underneath it, private-sector planning was up 26.2% while public-sector planning was down 20.6%. Same chart, opposite directions — and the gap between them is the whole story.

Private Projects are Carrying the Pipeline

On the private side, our team is having very different conversations than we were a year ago. Projects that had been quietly sitting on the shelf — owners and developers we’d been checking in with for months — are picking back up.

We’re confirming real movement on those plans now, not just intentions.

A lot of the new entries we’re publishing trace back to the same handful of themes: AI, data centers, energy, and manufacturing reshoring. These are large-scale, capital-intensive investments.

To put the scale in perspective, Office and Data Center starts were up roughly 400% year-over-year in dollar value, with January 2026 alone reaching $26.1 billion.

Power is a big part of that story too — utility and grid work is moving because electricity availability has become a gating issue for both digital infrastructure and industrial expansion.

And reshoring keeps adding new manufacturing projects as producers build domestic capacity and shorten their supply chains.

For firms tied to mission-critical facilities, site development, power systems, concrete, steel, mechanical systems and the specialty trades that support technically complex work, that is meaningful downstream opportunity — and it tends to show up first as planning intelligence, well before anything is shovel-ready.

So, the real question for 2026 isn’t whether opportunity is out there. It’s where it is, how durable it is, and whether it lines up with your capabilities, your geography and your customers.

This is shaping up to be a selective-growth year, not a rising-tide one.

Kristy O’Brien, Director of Content Acquisition, ConstructConnect

Public Planning is Losing Altitude

The public side is moving the other way. New public-sector planning entries were down 20.6%, and we’re feeling that on the front end.

Much of the federal and state stimulus work that drove our public-project verification over the last couple of years has already moved past early planning into design, bidding and active construction. That backlog is being worked through — it just isn’t being replenished at the same pace.

There are simply fewer brand-new public projects coming in to replace what’s completing.

That is not a collapse. Existing funded work is still very much active. But for contractors who lean heavily on public work, replacement opportunities may get harder to find unless state and local agencies refresh the pipeline with a new round of projects.

Growth is Narrower Than the Numbers Suggest

Here is the caution I would add. Even with private planning surging, only about half of all construction subcategories are forecast to expand through full-year 2026. A few very large private segments can produce eye-catching dollar gains without lifting the whole market with them.

So, the real question for 2026 isn’t whether opportunity is out there. It’s where it is, how durable it is, and whether it lines up with your capabilities, your geography and your customers. This is shaping up to be a selective-growth year, not a rising-tide one.

What It Means for Our Customers

For the people using our project intelligence tools, this comes down to pipeline strategy more than market sentiment.

A larger private planning pool tied to AI, power and reshoring rewards tracking projects earlier — especially where owner timelines, utility coordination and specialized scopes create long lead times before bids ever go out.

On the public side, I’d be careful about assuming past strength carries forward automatically. Existing work still supports backlog, but softer new entry could thin future opportunity if it stays that way.

The teams that do well this year will be the ones reading the mix, not just the headline — focusing coverage and pursuit on the construction segments that are actually gaining planning momentum.

That’s what we’ll keep doing on our end: gathering the data, confirming it with the people behind these projects, and getting it into your hands early enough to act on.

I’ll be back next quarter with more of what we’re seeing.

Stay Connected

Stay connected with ConstructConnect News for construction industry news and construction market analysis to stay ahead of what’s building next.

About ConstructConnect

At ConstructConnect, our software solutions provide the information that construction professionals need to start every project on a solid foundation. For more than 100 years, our keen insights and market intelligence have empowered commercial firms, building product manufacturers, trade contractors, and architects to make data-driven decisions, streamline preconstruction workflows, and maximize their productivity. Our newest offerings—including our comprehensive, AI-assisted software—help our clients find, bid on, and win more projects.

ConstructConnect operates as a business unit of Roper Technologies (Nasdaq: ROP), a constituent of the Nasdaq 100, S&P 500, and Fortune 1000.

For more information, visit constructconnect.com