KEY POINTS

-

Headline construction growth masks major disparities across subcategories and regions.

-

Data centers and select sectors drive gains while many categories decline.

-

Persistent material, energy, and labor pressures demand smarter, targeted strategies.

The top-line numbers for construction in 2026 tell only part of the story, and acting on them without digging deeper could cost you.

That was the central message from ConstructConnect Chief Economist Michael Guckes, who spoke at the company's recent Spring 2026 Construction Economy Outlook event.

"Which subcategories you decide to compete in, along with which geographies—those are the two most important things that will decide your company's future," Guckes told the audience.

Construction’s economic issues: Slow growth, stubborn inflation

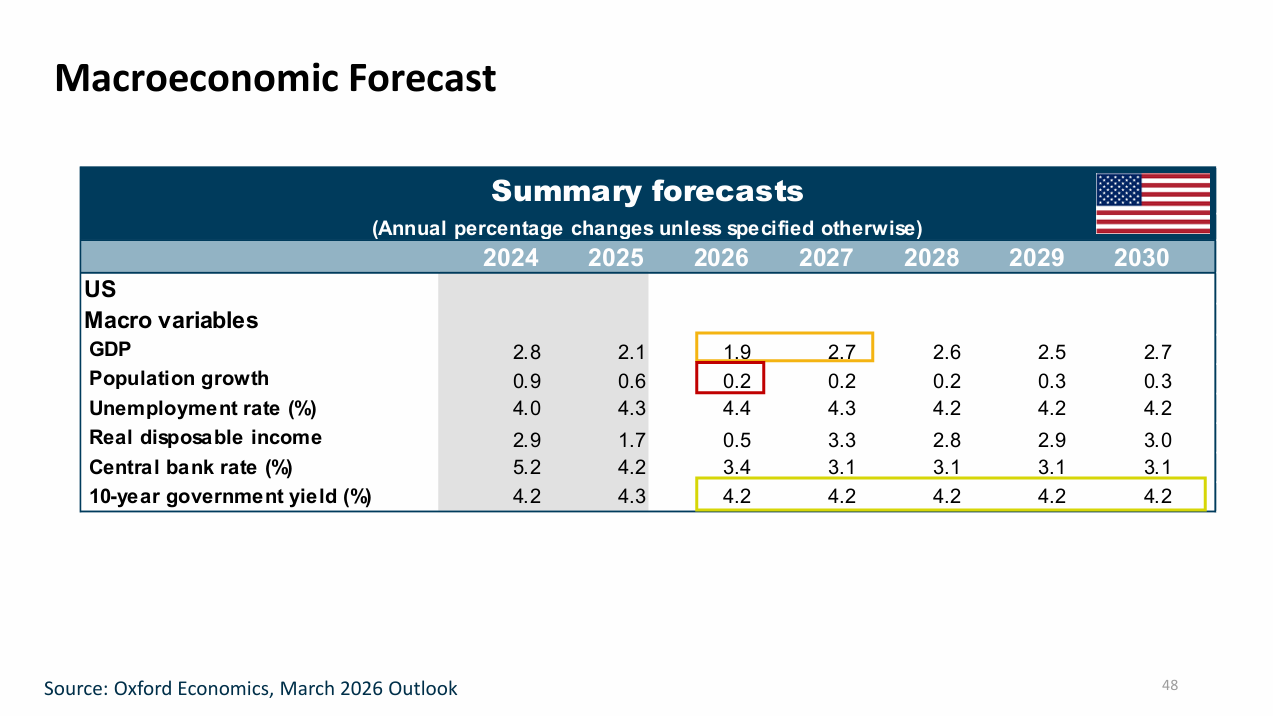

Looking at the bigger picture gives contractors reason to be selective. ConstructConnect forecasts U.S. Gross Domestic Product (GDP) growth of roughly 1.9% for the rest of the year, before it recovers toward 2.5–3% in subsequent years.

Population growth has dropped to 0.2% as immigration trends shift.  The ten-year government yield is holding near 4.2%, and with the Consumer Price Index (CPI) at 3.8%, rate relief from the Federal Reserve remains elusive. There’s even potential for the Fed to raise rates, according to Cleveland Federal Reserve President Beth Hammack, who said on June 2 that such an action may be needed if inflation does not come down.

The ten-year government yield is holding near 4.2%, and with the Consumer Price Index (CPI) at 3.8%, rate relief from the Federal Reserve remains elusive. There’s even potential for the Fed to raise rates, according to Cleveland Federal Reserve President Beth Hammack, who said on June 2 that such an action may be needed if inflation does not come down.

Where the growth in construction is concentrated

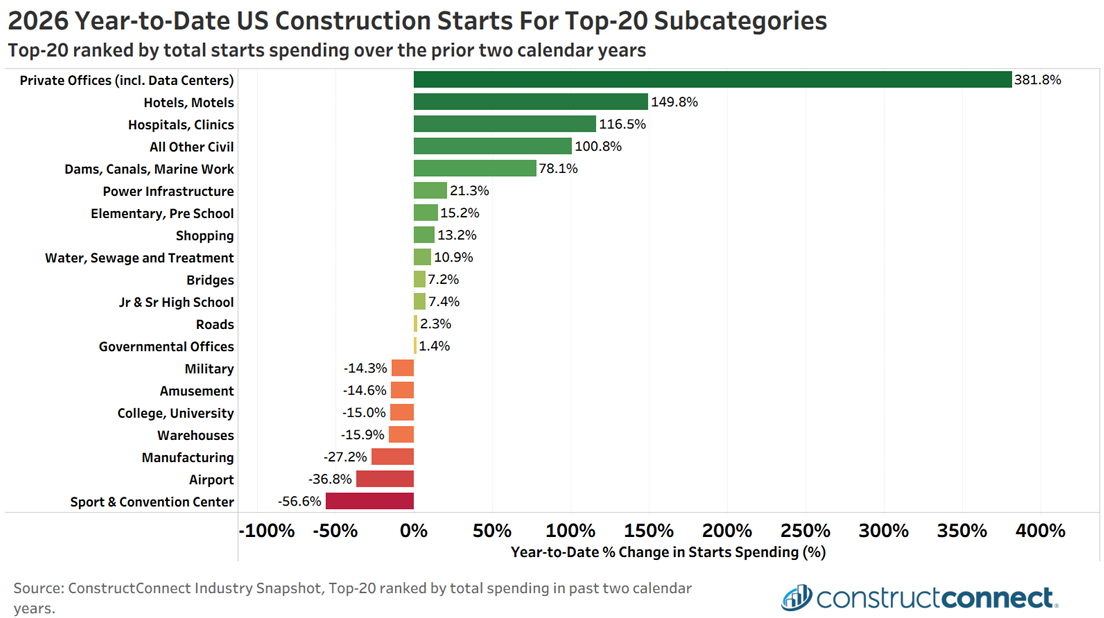

For firms willing to look past the headline figures, year-to-date starts data through March 2026 tell a more specific story. Data centers, which are counted within the “Private Offices” category, are up 380% compared to the same period in 2025. Hotels and motels are up 150%. Hospitals are up more than 115%.

For firms willing to look past the headline figures, year-to-date starts data through March 2026 tell a more specific story. Data centers, which are counted within the “Private Offices” category, are up 380% compared to the same period in 2025. Hotels and motels are up 150%. Hospitals are up more than 115%.

“Right around half of our subcategories are expected to grow, again, led by data centers,” Guckes said. “Of these, many of them will grow faster than the rate of construction.”

The data center surge is reshaping the industry's math. Data centers now account for 92% of all office-category construction dollars and 22% of total nonresidential building starts. That’s up from under 2% as recently as 2023.

Guckes projects $826 billion in office-category spending over the five-year forecast window, alongside a 55% increase in power infrastructure to support those facilities.

Removing the offices category from ConstructConnect's nonresidential building forecast entirely would flip the outlook from 1.5% growth to nearly a 9% contraction.

Reading the declines carefully

Not every down number signals a structural problem. Airports are down roughly 40% year-to-date and sports and convention centers are off more than 50%, but Guckes cautioned that several of these reflect corrections off unusually strong 2025 results and not deteriorating demand.

Guckes explained that even the mighty data center will see this shift eventually.

“The data center picture we see, starts peaking around 2029, maybe 2030,” he noted. “And so once we hit that peak, of course, data centers start to slow down. [It] doesn't contract. It's simply slowing down from the incredible surge that we, expect to see over the next few years.”

Materials and labor: The squeeze firms can't ignore

Whatever the subcategory, margin pressure is still a concern. Construction materials inflation is already near 6% and could climb higher as oil-driven energy costs continue feeding through the supply chain.

“[Energy prices have] fallen just a little bit in the last month, but not very much,” Guckes said. “And so, the question becomes one of ‘Well, clearly, construction inflation hasn't priced that in yet.’”

However, a White House revision on tariff policy earlier in the week could provide some relief; reducing tariffs on some aluminum, copper, and steel products.

“The clearest near-term takeaway for construction is that some imported equipment and building systems could become less expensive than they would have been under the prior rules,” ConstructConnect Associate Economist Devin Bell wrote in his article on the policy shift.

Compounding costs, labor productivity in both the U.S. and Canada is down, roughly 10% below 2019 levels. That’s what Guckes called a “structural headwind,” layered directly on top of rising material and energy costs.

“I think a lot of it is just going to come down to, being smart with how we use our labor [and] how we use investments in AI and other machinery and equipment to solve problems where we possibly can. There's so much more,” he advised.

The firms best positioned to navigate the next five years, Guckes suggested, will be those that resist managing to the averages.

"You don't want to just look at top-line numbers," he said. "You really need to get below the surface."

More insights from Guckes and the other leading economists that spoke at the Construction Economy Outlook can be found in our sister article on the ConstructConnect Blog, "What Construction Experts are Warning About the Industry, and What Contractors Should Do About it."

Stay Connected

Stay connected with ConstructConnect News for construction industry news and construction market analysis to stay ahead of what’s building next.

About ConstructConnect

At ConstructConnect, our software solutions provide the information construction professionals need to start every project on a solid foundation. For more than 100 years, our insights and market intelligence have empowered commercial firms, manufacturers, trade contractors, and architects to make data-driven decisions and maximize productivity.

ConstructConnect is a business unit of Roper Technologies (Nasdaq: ROP), part of the Nasdaq 100, S&P 500, and Fortune 1000.

For more information, visit constructconnect.com

.jpg)

.jpg)