KEY POINTS

-

US Nuclear regulators finalized 10 CFR Part 53, the first new reactor licensing framework since 1956, with officials estimating it could cut design review timelines to 18 months and application costs by half or more.

-

The technology-neutral rule enables factory-built reactors, siting adjacent to data centers and industrial facilities, and standardized designs.

-

The rule arrives as the electrification of the economy is surging, with ConstructConnect's March 2026 Data Center Report noting construction starts in the Power Infrastructure category surpassed $36 billion for the first time on record.

The US Nuclear Regulatory Commission (NRC) on March 25, 2026, finalized the first major overhaul of U.S. reactor licensing standards since 1956. The revised standards clear a path for faster, more cost-effective construction of advanced nuclear plants at a moment when electrification of the economy is pushing energy infrastructure investment to record levels.

The new rule, 10 CFR Part 53, replaces a licensing structure built around light-water reactor technology that produced only two commercially operational reactors since 1989.

Cut Time, Cut Costs, Expectations from Concept to Construction

NRC officials estimate it could cut design review timelines to 18 months or less and reduce application costs by half or more. A 2023 NRC draft regulatory analysis estimated net costs of $53.6 million to $68.2 million could be avoided, per applicant.

"This final rule is a major NRC action that provides a clear risk-informed, technology-inclusive licensing framework to enable new nuclear to safely move faster from concept to construction," NRC Chairman Ho Nieh said.

What Part 53 Changes for Advanced Reactor Licensing

Part 53 is technology-neutral, meaning it applies to any reactor type. The NRC states the rule, "Provides a broad and flexible regulatory framework that can be used for any reactor technology, any size reactor, and any commercial end-use."

Examples may include molten salt, gas-cooled, and small modular reactors, without requiring the case-by-case exemptions that have added years and millions of dollars under the old review framework.

The NRC completed the rule more than a year ahead of the end-of-2027 deadline set by the Nuclear Energy Innovation and Modernization Act of 2019. It was published in the Federal Register on March 30 and takes effect April 29.

Key provisions include:

-

Alternative siting criteria that allow reactors closer to load centers and industrial facilities.

-

Factory fuel loading that permits reactors to be fueled at the manufacturing site and shipped ready to operate.

-

Flexible staffing models for smaller or automated plants.

-

Standardized design pathways that let early projects establish a licensing basis for subsequent builds.

An image of U.S. power plant developers plans to add a record 86 gigawatts of new utility-scale generating capacity to the grid in 2026. That would surpass the 53 GW added in 2025, already the largest single-year installation since 2002. Image: U.S. Energy Information Administration

How Part 53 Impacts Construction Contractors and Manufacturers

Three features have direct implications for contractors, estimators, and building product manufacturers participating in related nonresidential construction projects.

1. Factory-built reactors shift work upstream.

Factory fuel loading compresses on-site construction timelines and could change sequencing of installers and logistics. This could expand the market for specialized fabrication and modular construction skilled firms.

2. Alternative siting opens new project locations.

Reactors can now be sited adjacent to data center campuses and industrial parks rather than only in more remote, lower-population areas. Reactors can now be co-located with the loads they serve. [Read more on behind-the meter-power]

3. Standardized designs mean repeatable programs.

Instead of one-off megaprojects, the rule supports the potential of more standardized builds with better predictability around scopes, schedules, and material requirements.

Nuclear Power Demand and Transformation in Global Energy

The regulatory easing tracks with expectations around a significant transformation in global energy consumption. The International Energy Agency's World Energy Outlook 2025 forecasts 40–50% growth in electricity demand by 2035.

The increase, the report said, is not driven by a single factor, but by broad electrification across multiple sectors, including artificial intelligence and data centers, advanced manufacturing, industrial heating and cooling, and electric transportation.

The Energy Information Administration separately reported that developers plan to add a record 86 gigawatts of new generating capacity to the grid in 2026. That figure exceeds the 53 GW added in 2025, which was already the largest single-year installation since 2002. Solar accounts for 51% of planned additions, followed by battery storage at 28%, and wind at 14%.

Data center construction is playing its part in energy transformation, particularly in the US nonresidential construction arena. ConstructConnect Chief Economist Michael Guckes reported that Data Centers, “accounted for nearly 90% of total Offices category spending in 2025.” The availability of adequate power infrastructure for these and future data centers is essential.

ConstructConnect's March 2026 Data Center Report noted that, “Construction starts in the Power Infrastructure category surpassed $36 billion for the first time on record.”

Related recent developments around nuclear power include:

-

Meta, Google, Amazon, and Microsoft have all signed nuclear power agreements or invested in reactor development.

-

Late in 2025, the American Nuclear Society reported that companies participating in the Department of Energy's Reactor Pilot Program are advancing at a remarkable speed.

-

In December, the US Department of Energy (DOE) announced the selection of two major project teams to support early deployment of small modular reactors, injecting $800 million into the effort.

-

More than a dozen advanced reactor developers are working with the NRC, and several have indicated interest in using Part 53 once it becomes available.

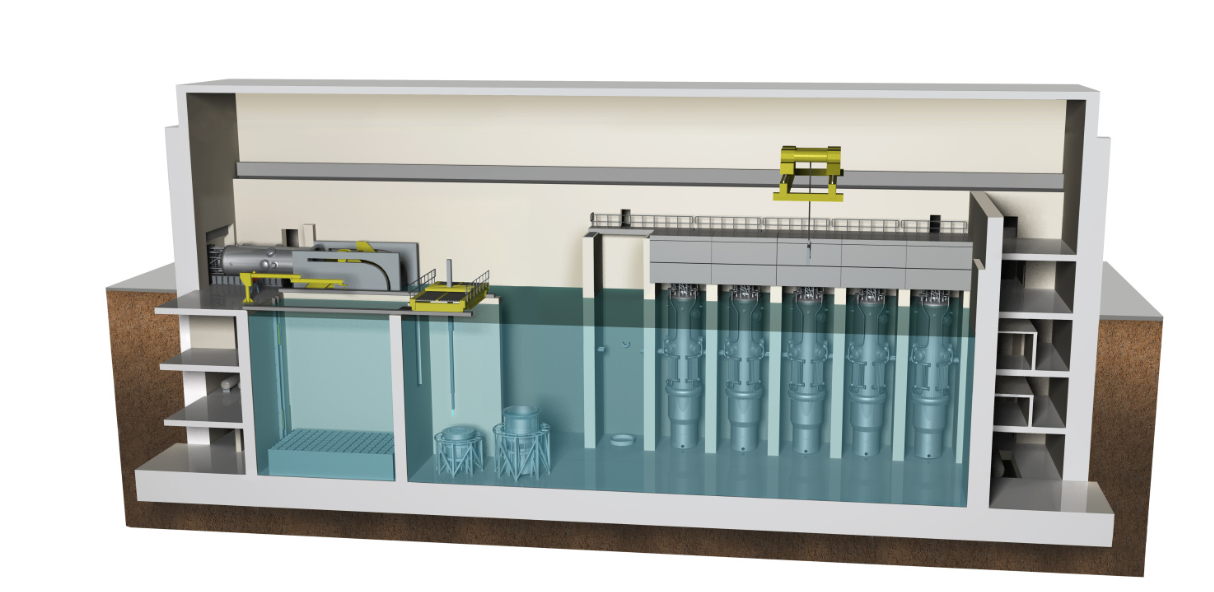

An illustration of a NuScale Power Reactor Building. An Advanced Small Modular Reactor (SMR) like these are compact nuclear power systems ranging from tens to hundreds of megawatts. Their smaller physical footprint and lower capital costs allow them to be sited in locations unsuitable for traditional large-scale nuclear plants, with the flexibility to add generating capacity incrementally. Image: US Department of Energy, NuScale Power Reactors.

The U.S. Nuclear Construction Pipeline

Between 1954 and 1978, the U.S. authorized construction of 133 nuclear reactors. Since then, only two, Georgia’s Vogtle Units 3 and 4, have been fully licensed and built from scratch under the modern regulatory framework.

Commercial nuclear power generation in the United States dates back to 1958. A total of 93 reactors operate across 54 plants in 28 states, with an average reactor age of roughly 42 years, according to the US Energy Information Administration.

The oldest active reactor is Nine Mile Point Unit 1 in New York and has been running since December 1969. The newest is Unit 3 at Georgia's Vogtle Electric Generating Plant, which entered commercial service on July 31, 2023, marking the first reactor to come online since Watts Bar 2 was commissioned in 2016.

Part 53 is the regulatory reset designed to reverse that trajectory which could channel the demand from electrification into a nuclear energy build pipeline.

Stay Connected

Stay connected with ConstructConnect News for construction industry news and construction market analysis to stay ahead of what’s building next.

About ConstructConnect

At ConstructConnect, our software solutions provide the information that construction professionals need to start every project on a solid foundation. For more than 100 years, our keen insights and market intelligence have empowered commercial firms, building product manufacturers, trade contractors, and architects to make data-driven decisions, streamline preconstruction workflows, and maximize their productivity. Our newest offerings—including our comprehensive, AI-assisted software—help our clients find, bid on, and win more projects.

ConstructConnect operates as a business unit of Roper Technologies (Nasdaq: ROP), a constituent of the Nasdaq 100, S&P 500, and Fortune 1000.

For more information, visit constructconnect.com